A sustainability report is an innovative tool used by companies to communicate to stakeholders the impact of their activities on the environment, people, and the economy.

It is a non-financial report that can be seen as an evolution of a financial report. In a sustainability report, organizations commit to annually reporting not only their economic performance but also their impact in the three spheres of sustainability: social, environmental, and economic.

The purpose of the report is to:

- Measure the company’s impact and move towards a responsible and sustainable profit generation.

- Communicate to all stakeholders the commitments made, the objectives set, and the results achieved in the field of Corporate Social Responsibility (CSR).

Benefits of a Sustainability Report:

- For the company:

- Improve strategies and long-term management policies.

- Compare and evaluate sustainability performance against laws, regulations, codes, performance standards, and voluntary initiatives.

- Simplify processes, reduce costs, and improve efficiency.

- Become a reference point for the territory and the community in which it operates.

- Affirm and confirm a positive reputation and demonstrate the reliability of the brand.

- For stakeholders:

- Increase transparency and accountability.

- Improve decision-making processes.

- Build trust and strengthen relationships with stakeholders.

The Corporate Sustainability Reporting Directive (CSRD):

The CSRD is a European directive that makes the preparation of a sustainability report mandatory for many companies.

It was published in the Official Journal of the European Union on 14 December 2022 and entered into force 20 days later. The text of the regulation describes the companies required to publish a sustainability report, the deadlines for doing so, and the criteria for drafting it.

The aim of the directive is to encourage organizations to undertake structured, measurable, and comparable approaches to their sustainability actions to combat greenwashing and guide organizations towards a sincere awareness of the importance of responsible growth.

Which companies must prepare a Sustainability Report and by when?

The companies will be required to publish a sustainability report at different times. The deadlines vary depending on the type of company and some size criteria.

According to the CSRD, the companies that will have to publish an environmental, social, and governance sustainability report are:

- European companies listed on financial markets (including SMEs, only micro-enterprises are excluded).

- Large European unlisted companies.

- Non-European companies.

Large unlisted companies are companies that meet at least two of these three criteria:

- Turnover of more than 50 million euros.

- Net assets of more than 20 million euros.

- More than 250 employees.

The companies will be required to publish a sustainability report at different times.

The first will be large companies, i.e. companies with more than 500 employees, which will publish the report from 1 January 2025. These are companies that were already subject to the previous directive (NFRD), so they are already familiar with this type of report. The first companies will have to apply the new rules for the first time with reference to the 2024 financial year, for reports published in 2025. The last to publish the sustainability report will be non-European companies, which will have to do so from 2029.

How to prepare a Sustainability Report?

The directive requires companies to report on their performance and the indicators they use to measure it (KPIs), in relation to the resilience of their strategy to sustainability risks.

The first core element that the directive requires to be reported on is the materiality, or rather the double materiality, of the company. Double materiality refers to the two-way impact, both of the company on the outside world and of the outside world on the company’s finances.

To meet this criterion, it is necessary to carry out an analysis of what is considered material for the company and what is not, in order to then prioritize and work on the actual materialities. Material for a company are the most relevant environmental, social and governance impacts (positive and negative). The materiality analysis is nothing more than the voting of the positive impacts of a company on the environment, people and economy.

Once the material impacts have been identified, they are grouped into themes and the GRI indicators to be included in the report are chosen. In theory, all material impacts should be covered by an indicator.

Characteristics of the Sustainability Report:

The European Commission has defined common standards that will help companies communicate and manage their sustainability performance efficiently, reliably, and comparably.

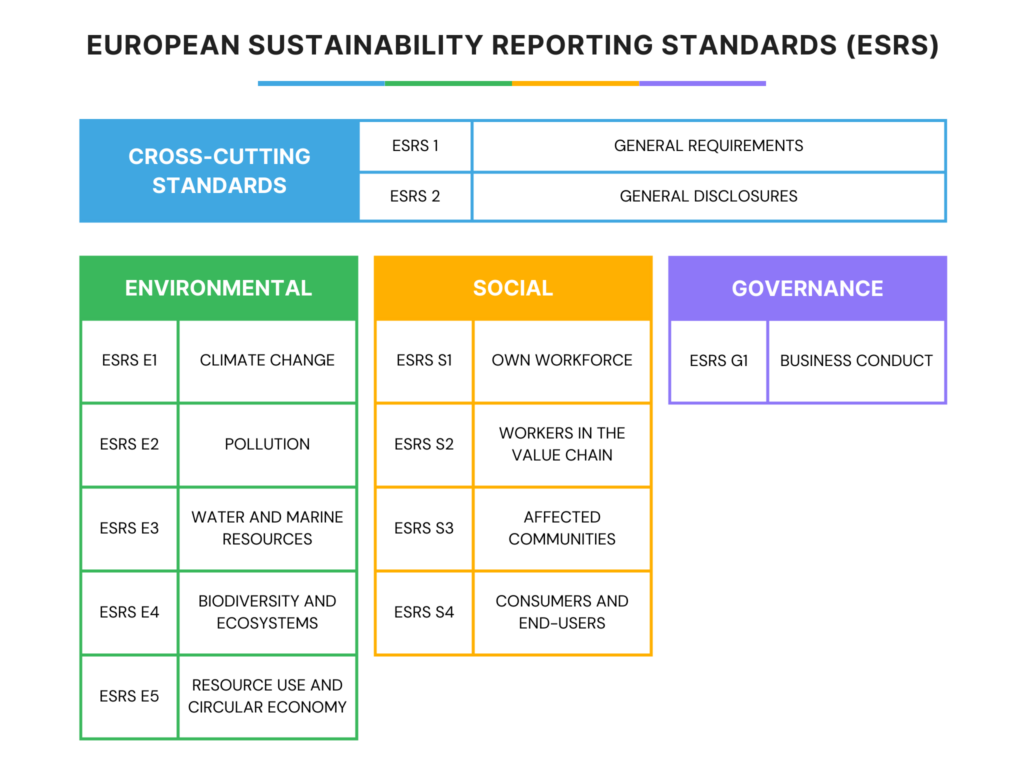

Companies subject to the CSRD will have to report according to the European Sustainability Reporting Standards (ESRS). The ESRS specify the information that a company must disclose regarding its material impacts, risks, and opportunities related to environmental, social, and governance (ESG) sustainability.

There are three categories of ESRS:

1. Cross-cutting standards:

These establish the general principles to be applied when reporting. They are mandatory for all companies subject to the CSRD.

2. Topical standards:

These specify the essential information to be communicated and are mandatory for all companies subject to the CSRD. They cover environmental, social, and governance (ESG) topics.

3. Sector-specific standards:

These can be included or not, depending on the outcome of the materiality analysis. The company will only report the relevant information and may omit information that is not relevant to its business model and activities.

The three categories of ESRS are designed to:

- Ensure that companies report on the most relevant sustainability issues.

- Provide a consistent framework for reporting, which will make it easier for stakeholders to compare companies’ performance.

- Help companies to improve their sustainability performance.

The ESRS are a significant step forward in the development of sustainable reporting. They will provide companies with a clear framework for reporting on their sustainability performance and will help stakeholders to make more informed decisions.